BMO - How to invest responsibly in the emerging market dairy industry

06 Jul 2021

Discover how human activity threatens the ocean and how investors can drive sustainable solutions.

The demand for dairy in developed markets may be declining, but there is still a runway for growth in many emerging markets. The dairy industry can positively support social issues such as health and wellbeing – the ‘S’ in ESG – but it also has negative environmental impacts – the ‘E’ in that same acronym. So we’re asking: can this industry reduce its negative impact to become a sustainable part of meeting the nutritional needs of future populations in emerging markets?

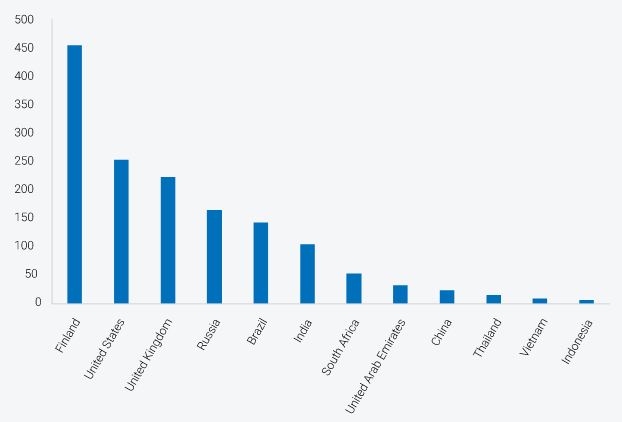

Increasing demand for dairy in emerging markets

Combined with rising incomes and urbanisation, the demand growth for protein rich and convenience food looks set to grow rapidly. And dairy companies are well placed to capture this growth. Don’t just think a glass of milk – think yoghurt, ice cream and cheese… all products that will allow ample room for diversification and premiumisation. In many emerging markets, the dairy industry is still in the early stages of consolidation, leaving room for the best players to gain market share.

Source: Food & Agriculture Organisation of the United Nations, 2020

Dairy and the UN Sustainable Development Goals (SDGs)

Cow’s milk is a widely distributed, good source of protein and calcium, as well as nutrients such as vitamin B12, iodine and magnesium. It is likely to play an important role in helping countries, particularly those in the developing world, address malnutrition challenges and meet SDG 2: Zero Hunger. According to the UN, the dairy sector accounts for about 14% of global agricultural trade, and more than 150 million farmers (most of them small) depend on tending to cows for their livelihood. We therefore see the dairy industry not just as an enabler of food security and nutrition, but also of sustained economic growth and inclusive social development.

What about the environmental impacts?

At the same time, we must acknowledge the significant environmental impacts of dairy farming. Increasing demand for dairy products around the world is putting significant pressure on the natural resources that make this industry possible, particularly water and soil. Dairy cows and their manure also produce significant amounts of methane and other greenhouse gas emissions that contribute to climate change. Meanwhile, poorly handled manure and fertilisers can degrade local water resources, and unsustainable dairy farming and feed production practices can lead to the loss of ecologically important areas. Overall, these factors can contribute to the growing problem of biodiversity loss, which you can read more about here.

Great strides have already been made to reduce the environmental impact of dairy farms. According to the US Sustainability Alliance, milk production in the US has quadrupled in the last 60 years, but a gallon of milk today uses 65% less water and greenhouse gas emissions have been reduced by 63%. Progress continues to be made e.g. the World Wildlife Fund’s Net Zero Initiative, but there is still considerable room for improving the sustainability of the industry.

Our responsible investment approach

It is our responsibility to consider all relevant factors that could materially impact the sustainability of a company’s business model. Therefore, the evaluation of ESG opportunities and risks is integral to our process. We look at how our companies are mitigating the risks and maximising the opportunities to maintain and enhance their license to operate over the long term. A deeper understanding of material risks and opportunities allows us to ask the right questions, understand our companies’ answers, analyse their current strategy and compare to best practice.

Indicators of good practice that we look for in our initial analysis across companies in all sectors include:

- Are material environmental and social considerations incorporated into long-term business strategies?

- What is the governance structure? Responsibility and accountability for material ESG issues should sit at board and senior management level, and incentives should be aligned across the business, with strong environmental and social targets and performance indicators.

- Are profits realistic? Supply chain profit squeezing can be a sign of short-term thinking/corners being cut.

- Do the key decision-makers act with integrity? We meet management as well as looking at their track record. Are they making decisions for the long-term sustainability of the business and not just hitting 3-year profit goals?

- Is the company moving towards best practice? We do not expect our emerging market companies to be at the forefront of ESG management (although some of them are), but we do expect them to be open to improve. We want to know where they are now and whether they are taking sufficient action to get to where they need to be.

- Does the company report on its ESG practices and performance? High standards of ESG reporting have become critical for accurate investor information, public discourse, and regulatory guidance. They allow companies to present a comprehensive sustainability and value creation story.

- How many ESG-related incidents has the company been involved in, and how has it responded to those?

- How well do they know their supply chain? Are operations in high risk climate change/water areas and have the company mapped their supply chain. Do they work with farmers to improve practices?

Regarding the dairy industry in particular, plans and actions to mitigate the negative environmental impacts of milk production are important considerations for us when making our initial assessment of a dairy company, and will continue to be top of our mind throughout our investment process, including portfolio construction and active ownership.

Engaging for positive change

Our obligations don’t end when an investment decision is made. We engage with our investee companies to encourage robust ESG practices that will help them create long-term shared value.

In this context, we have asked our companies in the dairy industry, including China Mengniu, Yili Group and Vietnam Dairy Products to:

- Fully incorporate climate change and other environmental considerations into long-term business strategies

- Set science-based carbon emissions reduction targets that cover emissions from the entire dairy value chain

- Collaborate with farmers to develop and implement sustainable agricultural practices, including around manure, soil and waste management

- Map environmental risks and opportunities to raw milk and feedstock supply chains

- Explore and invest in alternatives to plastic packaging

Final thoughts

Like most areas of life, investing in the dairy industry is not black and white. When we consider the growing challenges of malnutrition and food accessibility, a relatively cheap, protein-rich source of food cannot be discounted. Demand growth in the developing world is an exciting investment opportunity. However, as custodians of capital we must have a comprehensive understanding of the challenges and risks in the sector too. Engagement to encourage best practices and sustainable production can help to mitigate these risks and move towards reducing the industry’s impact on the environment.

Risk Warning

The value of investments and any income derived from them can go down as well as up and investors may not get back the original amount invested. Investing in emerging markets is generally considered to involve more risk than developed markets. BMO Global Asset Management’s voting, engagement and public policy work is conducted independently of the wider BMO Financial Group. Positions taken by BMO Global Asset Management may not be representative of the views of the BMO Financial Group as a whole or of the other lines of business within it. Views and opinions have been arrived at by BMO Global Asset Management and should not be considered to be a recommendation or solicitation to buy or sell any companies that may be mentioned. The information, opinions, estimates or forecasts contained in this document were obtained from sources reasonably believed to be reliable and are subject to change at any time.

July 2021

Please note that these are the views of Emerging Markets Team of BMO Global Asset Management and should not be interpreted as the views of FPIL.